In these times, double down — on your skills, on your knowledge, on you. Join us Aug. 8-10 at Inman Connect Las Vegas to lean into the shift and learn from the best. Get your ticket now for the best price.

Turmoil in the banking system may serve as the catalyst for a modest recession, but it’s likely to resemble the savings and loan crisis of the 1980s more than the 2008 financial crisis, Fannie Mae economists said Friday.

The failures of Silicon Valley Bank and Signature Bank could prove to be a double-edged sword for housing — providing a tailwind for home sales in the form of lower mortgage rates but also prompting small and midsized regional banks to tighten lending standards, Fannie Mae economists said in their latest monthly economic and housing forecasts.

“While home sales experienced a large bump in February following a pullback in mortgage rates … recent mortgage application data suggest that last month’s level of home sales will be temporary,” Fannie Mae economists said. Ongoing banking instability “may affect the availability of jumbo mortgages and residential construction loans due to the high concentration of those originations stemming from small and midsized banks.”

Forecasters with Fannie Mae’s Economic and Strategic Research Group published their latest monthly forecast Friday, but the numbers were finalized on March 13 — just days after the failures of Silicon Valley Bank and Signature Bank and more than a week before the Federal Reserve’s March 22 meeting.

Economists at the mortgage giant say recent turbulence in the banking sector adds some uncertainty to their forecast but doesn’t fundamentally change their baseline outlook.

Fannie Mae economists have been predicting a 2023 recession since last April. But stronger-than-expected economic data have pushed back the anticipated start of the recession from the second quarter to the second half of this year, they said.

“Regardless of how the banking turbulence plays out, we continue to expect home sales activity to remain subdued for the remainder of 2023,” Fannie Mae economists said in commentary accompanying their forecast. “Even if mortgage rates were to pull back to 6 percent, affordability remains highly constrained. Additionally, most existing mortgage borrowers will continue to have rates well below current market rates. This ‘lock in’ effect, where existing homeowners are hesitant to give up their low mortgage rates, remains a strong disincentive to move to a new home.”

Source: Fannie Mae Housing Forecast, March 2023

Fannie Mae forecasters now expect 2023 home sales to decline by 18 percent to 4.627 million. Sales of existing homes are expected to fall by 20 percent to 4.019 million, with sales of new homes dipping by 5 percent to 608,000.

While home sales are on track for a stronger-than-expected first quarter, Fannie Mae economists expect a larger contraction later in the year.

“Many homebuyers who may have been waiting on the sidelines appear to have jumped in as existing home sales increased 14.5 percent in February, modestly more than we expected based on previous increases in mortgage application data,” Fannie Mae economists said. “However, recent mortgage activity points to that level of home sales being temporary, and we expect lower numbers in March.”

Next year, the latest forecast is for home sales to rebound 7 percent to 4.955 million, driven by 8 percent growth in sales of existing homes to 4.34 million.

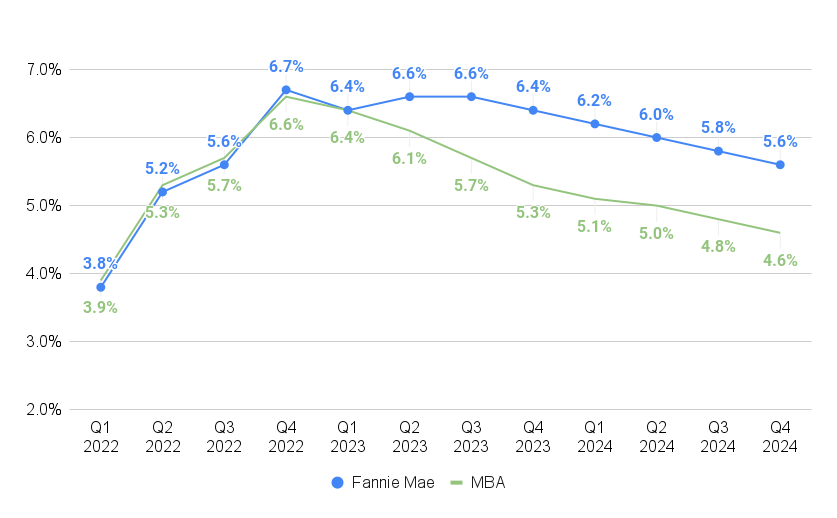

Source: Fannie Mae and Mortgage Bankers Association forecasts

While Fannie Mae economists had expected rates on 30-year fixed-rate mortgages to average 6.6 percent during the second and third quarters, that forecast was completed before rates came down in the aftermath of the Federal Reserve’s first meeting following the failures of Silicon Valley Bank and Signature Bank.

Fed policymakers voted to raise the short-term federal funds rate by 25 basis points on Wednesday, but Federal Reserve Chair Jerome Powell said events in the banking system over the past two weeks are likely to result in tighter credit conditions for households and businesses. Policymakers will want to see the latest data before hiking rates again, Powell said.

The Fed’s more dovish stance was largely expected; and by Thursday, rates on 30-year fixed-rate mortgages had already fallen to 6.34 percent — down half a percentage point from a 2023 high of 6.84 percent on March 8, according to rate lock data compiled by Optimal Blue.

Fannie Mae economists acknowledged that the recent sharp drop in long- and intermediate-term interest rates means their mortgage rate forecast could underestimate the potential for rates to come down this year and next.

In a March 20 forecast, economists at the Mortgage Bankers Association predicted rates on 30-year fixed-rate loans will average 5.3 percent during the final three months of the year and slide to 4.6 percent by the fourth quarter of 2024.

Lower rates could also provide a tailwind for home sales and mortgage originations, Fannie Mae economists said. But lower rates won’t be of much help if borrowers can’t get loans in the first place.

“While we do not know how long-lasting the current banking concerns will be, banks have borrowed a record amount from the Fed’s discount window over this past week, while Federal Home Loan Bank advances have also surged,” Fannie Mae economists warned. “This is a clear sign of liquidity stress among many regional banks who may be facing deposit run pressure. We anticipate this will stabilize, but it is likely to result in greater reluctance to lend as banks seek to preserve liquidity. ”

If that happens, Fannie Mae projects that homebuyers seeking jumbo mortgages be among those most affected. As of February 2022, jumbo loans exceeding Fannie Mae and Freddie Mac’s conforming loan limit (currently $726,200 in most parts of the country) accounted for approximately 12 percent of all loans originated.

“Unlike conforming loans, which are largely financed through mortgage-backed securities (MBS) via capital markets, the jumbo mortgage space is almost entirely funded via the banking sector, and some regional banks are more concentrated in jumbo mortgage lending than others,” Fannie Mae forecasters warned. “Ongoing liquidity stress could limit home financing and therefore sales in the related market segments and geographies with high jumbo concentration.”

In the long run, tightening of lending standards at midsized regional banks could also slow the construction of homes and apartments.

“Like jumbo mortgage lending, construction and development loans both for single-family construction and multifamily construction are heavily financed by regional and community banks specializing in this area,” Fannie Mae forecasters noted. “Small and midsized banks, defined as those with fewer domestic assets than the top 25 banks, account for approximately two-thirds of total bank-financed commercial real estate loans. We would therefore expect a drag on housing starts and multifamily residential sales.”

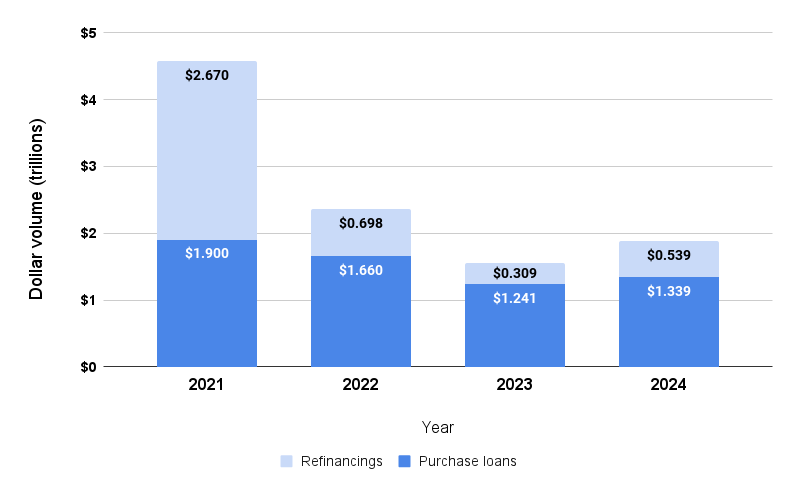

Purchase mortgage lending expected to contract by 25 percent

Source: Fannie Mae Housing Forecast, March 2023

The prospect of a slowdown in home sales prompted Fannie Mae economists to trim their forecast for 2023 purchase loan mortgages by $76 billion to $1.241 trillion. That would represent a 25 percent drop from a year ago.

While Fannie Mae is projecting that purchase loan originations will rebound by 8 percent next year, to $1.339 trillion, that’s $106 billion less than the forecast issued in February.

Thanks to last year’s dramatic rise in mortgage rates, mortgage refinancing volume is expected to shrink by 56 percent this year to $309 billion, but grow by 74 percent next year to $539 billion.

With mortgage rates down since that forecast was put together, Fannie Mae economists say mortgage originations could come in stronger than expected.

Get Inman’s Extra Credit Newsletter delivered right to your inbox. A weekly roundup of all the biggest news in the world of mortgages and closings delivered every Wednesday. Click here to subscribe.